FRM: Implied volatility smile

9:35

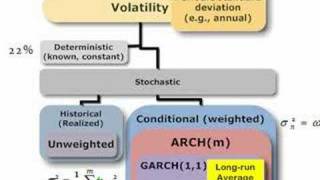

FRM: Volatility approaches

1:20:15

Ses 3: Present Value Relations II

16:40

Implied Volatility Skew & Three Things it Can Tell You

10:00

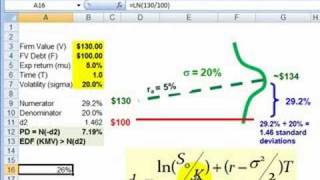

FRM: How d2 in Black-Scholes becomes PD in Merton model

8:51

FRM: Lognormal value at risk (VaR)

7:06

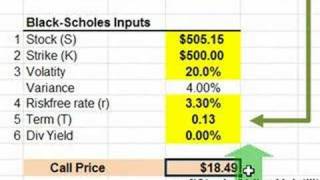

FRM: Implied volatility

21:56

Risk-neutral probabilities (FRM T5-07)

25:57