Risk-neutral probabilities (FRM T5-07)

27:20

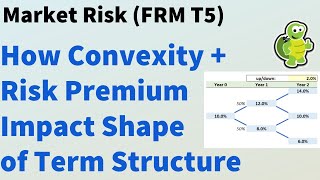

Convexity and risk premium impacts on shape of term structure (FRM T5-08)

3:05:45

Hands-On Power BI Tutorial 📊Beginner to Pro [Full Course] ⚡

32:13

Expected shortfall: approximating continuous, with code (ES continous, FRM T5-03)

10:12

Risk neutral probability measure simplified

24:44

Stochastic Calculus for Quants | Risk-Neutral Pricing for Derivatives | Option Pricing Explained

22:23

4 2 Risk neutral pricing Part 1

21:26

Value (VaR) Mapping a fixed-income portfolio (FRM T5-05)

3:02:18