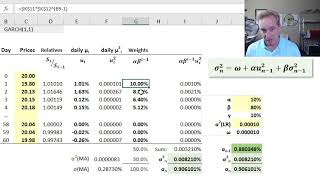

FRM: GARCH(1,1) to estimate volatility

8:56

FRM: Exponentially weighted moving average (EWMA)

27:07

How to estimate arch model - eviews tutorial complete

22:29

Value at Risk (VaR) Backtest (FRM T5-04)

10:25

GARCH Model : Time Series Talk

14:45

Volatility: GARCH 1,1 (FRM T2-23)

1:07:00

Sezen Aksu En Sevilen Şarkıları (1 Saat)

1:03:37

Sade - Ultimate

22:22