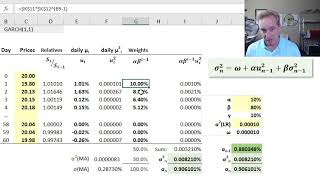

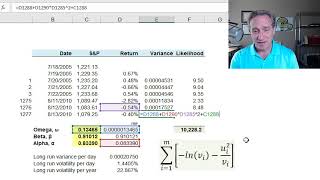

FRM: GARCH(1,1) to estimate volatility

8:56

FRM: Exponentially weighted moving average (EWMA)

22:22

GARCH model - volatility persistence in time series (Excel)

14:45

Volatility: GARCH 1,1 (FRM T2-23)

21:11

Estimate Volatility - Exponentially Weighted Moving Average (EWMA) - FRM

9:02

Calculating VAR and CVAR in Excel in Under 9 Minutes

55:51

ARCH model

27:07

How to estimate arch model - eviews tutorial complete

12:12