Volatility: Exponentially weighted moving average, EWMA (FRM T2-22)

14:45

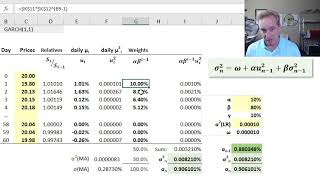

Volatility: GARCH 1,1 (FRM T2-23)

21:11

Estimate Volatility - Exponentially Weighted Moving Average (EWMA) - FRM

18:02

Three approaches to value at risk (VaR) and volatility (FRM T4-1)

14:43

Efficient Frontier Explained in Excel: Plotting a 3-Security Portfolio

1:15:33

Ferdi Özbeğen - Can Suyum (Full Albüm)

14:24

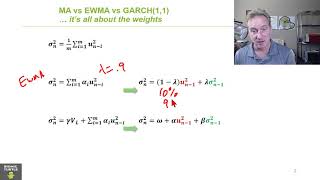

Comparing volatility approaches: MA versus EWMA versus GARCH (FRM T2-25)

28:52

Build A Full Discounted Cash Flow Model for a REAL Company

30:28