2.3) Why Trading Optimizations need a Statistically Significant Sample Size (Number of Trades)

1:57

2.4) How to Extract Optimal Parameter Values in Optimizations using Statistical Power Analysis

6:11

2.2) Using Statistical Power Analysis to determine Sample Size in Trading Optimizations & Backtests

11:43

6.2) Reduce Noise Overfitting by Reducing the Degrees of Freedom in Optimizations

54:22

How to Troubleshoot Kubernetes Clusters | Kubernetes Tutorial | K21Academy

5:36

9.1) The Importance of Choosing Robust Performance Metrics / Criteria in Trading Optimizations

10:37

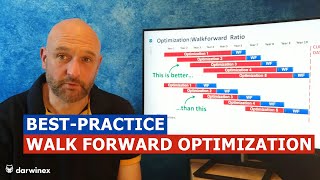

13.1) Walk Forward Analysis Best-Practice | Improving your Trading Strategy Optimizations

10:29

6.3) Real Example: How Over-Fitting occurs when Increasing Degrees of Freedom

8:12