Value (VaR) Mapping a fixed-income portfolio (FRM T5-05)

19:01

Rank Correlations: Spearman's and Kendall's Tau (FRM T5-06)

22:29

Value at Risk (VaR) Backtest (FRM T5-04)

21:56

Risk-neutral probabilities (FRM T5-07)

26:41

Lognormal value at risk (VaR, FRM T5-01)

43:46

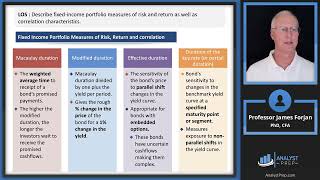

Overview of Fixed-Income Portfolio Management (2025 Level III CFA® Exam – Reading 10)

33:37

Something Strange Happens When You Trust Quantum Mechanics

14:17

How the Elite rigged Society (and why it’s falling apart) | David Brooks

8:34