Replicating Portfolio - Call Option

1:46:33

FINANCE . LES OPTIONS . MODELE BINOMIAL DE COX-ROSS-RUBINSTEIN

16:51

Binomial Options Pricing Model Explained

38:47

Option Replication Using Put-Call Parity (2024/2025 Level I CFA® Exam – Derivatives – Module 9)

8:14

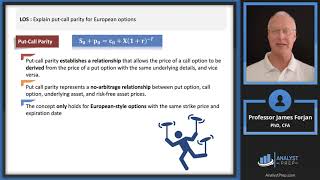

CFA Level I Derivatives - Put-Call Parity

10:24

Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

2:00:26

Lecture 11 Option pricing - Replicating portfolio method

8:42

CFA Level I Derivatives - Derivative Pricing and Replication

44:21