How to interpret N(d1) and N(d2) in Black Scholes Merton (FRM T4-12)

18:10

Option delta (FRM T4-13)

5:48

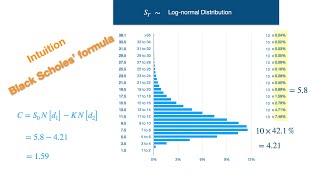

An intuitive explanation the Black Scholes' formula

11:53

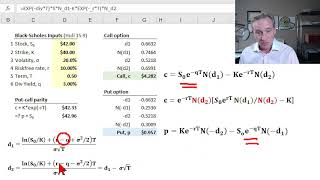

Black Scholes Merton option pricing model (FRM T4-11)

10:00

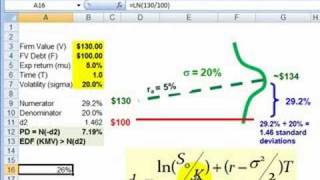

FRM: How d2 in Black-Scholes becomes PD in Merton model

10:24

Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

18:39

Can you crack this beautiful equation? – University exam question

9:23

Black Scholes Option Pricing Model Explained In Excel

12:57