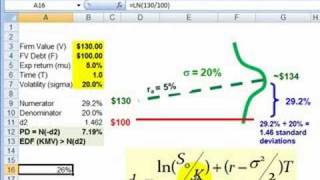

FRM: Expected default frequency (EDF, PD) with Merton Model

6:53

FRM: Intro to Credit: Adjusted Exposure

10:00

FRM: How d2 in Black-Scholes becomes PD in Merton model

8:57

FRM: Logistic distribution maps credit score to probability of default (PD)

32:13

Expected shortfall: approximating continuous, with code (ES continous, FRM T5-03)

12:51

Moody's KMV Model

17:04

Expected shortfall (ES, FRM T5-02)

15:26

Luciano Rezende Ambientes Saudáveis em Áreas Urbanas

9:16