DCC GARCH model: Multivariate variance persistence (Excel)

20:30

Is Phillips curve still relevant? Chow structural break test explained (Excel)

22:22

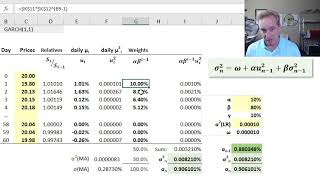

GARCH model - volatility persistence in time series (Excel)

13:01

Introduction to DCC - Dynamic Conditional Correlation Models

15:48

MG#5 Correlation and Covariance in DCC GARCH Model in R Studio

13:44

EGARCH model: exponential asymmetric volatility persistence (Excel)

22:24

Value-at-risk (VaR) - variance-covariance and historical simulation methods (Excel) (SUB)

14:45

Volatility: GARCH 1,1 (FRM T2-23)

10:03