Coherent risk measures and why VaR is not coherent (FRM T4-5)

23:25

Introduction to binomial option pricing model: two-step (FRM T4-6)

18:02

Three approaches to value at risk (VaR) and volatility (FRM T4-1)

11:52

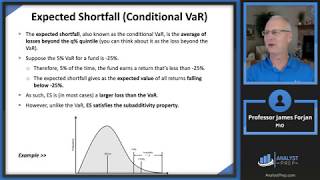

Expected Shortfall & Conditional Value at Risk (CVaR) Explained

8:47

VaR and Stress Tests - Financial Markets by Yale University #4

18:20

Measures of Financial Risk (FRM Part 1 2025 – Book 4 – Chapter 1)

23:39

O movimento divino de Bobby Fischer leva o mundo inteiro do xadrez ao colapso! | "Jogo do século"

18:27

Forget Doping, These GENIUS Cheaters Will Blow Your Mind

19:44