Monte Carlo Variance Reduction with Control Variates | Option Pricing Accuracy

21:07

Why Gamma still matters for Monte Carlo Variance Reduction?

27:14

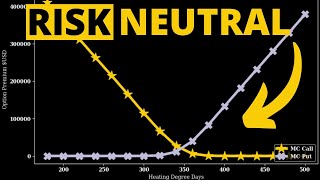

Risk Neutral Pricing of Weather Derivatives

13:25

Monte Carlo Variance Reduction with Antithetic Variates | Option Pricing Accuracy

12:25

Simulating the Heston Model with Python | Stochastic Volatility Modelling

15:32

Monte Carlo Integration In Python For Noobs

27:02

Barrier Option Pricing with Binomial Trees || Theory & Implementation in Python

33:22

Variance reduction methods

16:44