Lognormal property of stock prices assumed by Black-Scholes (FRM T4-10)

11:53

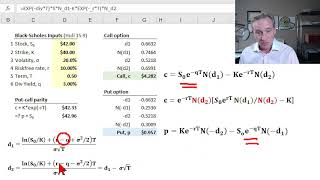

Black Scholes Merton option pricing model (FRM T4-11)

31:22

The Trillion Dollar Equation

18:56

Coherent risk measures and why VaR is not coherent (FRM T4-5)

6:44

Log normal distribution | Math, Statistics for data science, machine learning

18:10

Option delta (FRM T4-13)

13:49

Dos grandes mentiras económicas que todavía crees | Economía Explicada

12:28

Why are Stock Prices Lognormal?

10:24