Expected shortfall: approximating continuous, with code (ES continous, FRM T5-03)

22:29

Value at Risk (VaR) Backtest (FRM T5-04)

46:03

Level 1 Chartered Financial Analyst (CFA ®): Common Probability Distributions

9:02

Calculating VAR and CVAR in Excel in Under 9 Minutes

34:59

How to Use Excel Like a Data Analyst: Master Data Modeling, Cleaning, and Analysis

42:36

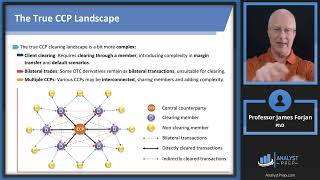

Central Clearing (FRM Part 2 – Book 2 – Credit Risk Measurement and Management – Ch 18)

2:16:49

Deha 14. Bölüm

11:52

Expected Shortfall & Conditional Value at Risk (CVaR) Explained

57:29