Heston Model Calibration in the "Real" World with Python - S&P500 Index Options

12:25

Simulating the Heston Model with Python | Stochastic Volatility Modelling

30:09

Monte Carlo Simulation for Option Pricing with Python (Basic Ideas Explained)

14:55

Heston model explained: stochastic volatility (Excel)

8:53

How AI Got a Reality Check

27:14

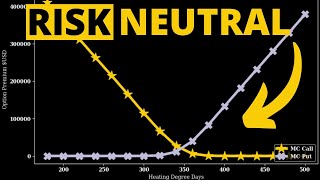

Risk Neutral Pricing of Weather Derivatives

16:12

QUANT FINANCE 1 - Why We Never Use the Black Scholes Equation, 1

16:29

Understanding Market Makers || Optiver Realized Volatility Kaggle Challenge

7:40