FRM: Lognormal distribution

21:49

Lognormal property of stock prices assumed by Black-Scholes (FRM T4-10)

8:51

FRM: Lognormal value at risk (VaR)

9:21

FRM: Normal probability distribution

8:32

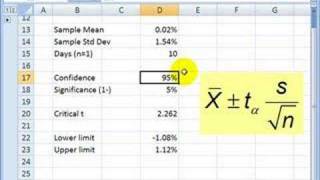

FRM: Student's t distribution

8:56

FRM: Exponentially weighted moving average (EWMA)

6:18

FRM: Why we use log returns in finance

8:45

Distribution moments

9:28